Inventory as a Dynamic Risk Asset: Implications for Lending & Recovery

This article was originally published in the March 2026 issue of Turnaround Management Association’s Journal of Corporate Renewal magazine.

Traditionally, the relationship between inventory cost basis and realizable value has been relatively predictable. Thanks to tariff-driven cost shocks, supply-chain reconfiguration and delayed pricing responses, that’s no longer the case. For many companies, inventory—long viewed as a stabilizing asset in periods of stress — is increasingly becoming a source of valuation risk. Margin compression, uneven pricing power, and rapidly shifting input costs are undermining assumptions that historically supported both lending decisions and recovery planning.

In this environment, annual cost updates and standardized inventory accounting systems are often failing to capture rapid cost inflation. Tariffs, freight disruption and supplier restructuring have introduced volatility that balance sheets are slow to reflect. As a result, inventory valuations that may appear sound according to historical metrics run the risk of overstating realizable value.

These dynamics are reshaping recovery outcomes across valuation, lending and restructuring, with uneven impacts by sector, company size and SKU mix. In many cases, the challenge is not simply higher costs, but a growing divergence between recorded cost and exit pricing—the gap between what companies paid for inventory and what they can reasonably be expected to recover.

A Volatile Cost Environment

Over the past year, tariffs have shifted from being a static input to a constantly shifting variable, subject to political negotiation, carve-outs, exclusions and sudden escalations. Dollar amounts and effective rates remain in flux, complicating planning, pricing and valuation.

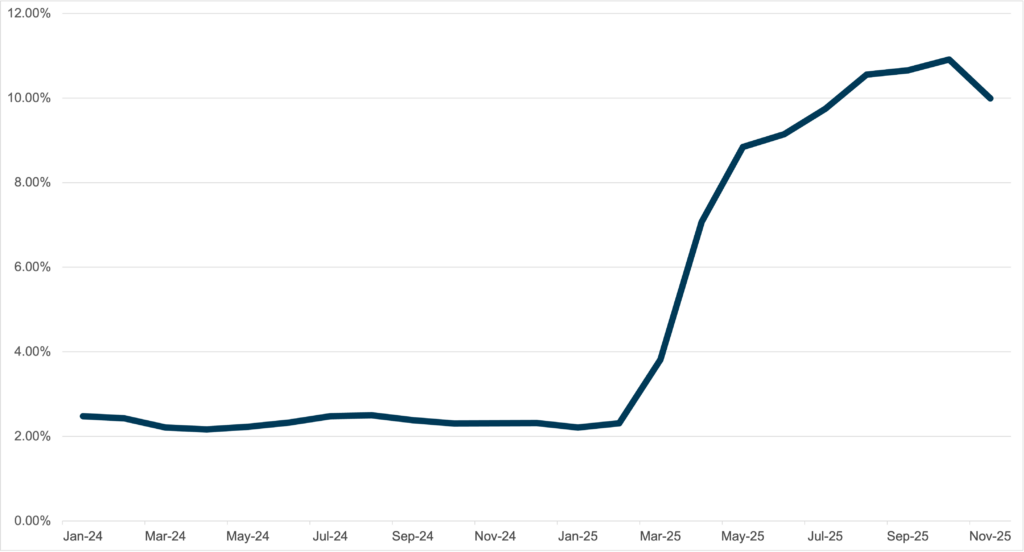

Figure 1 shows the variation in average tariff rates by month since January 2024. In 2025, average rates rose all months but one through November 2025—though not always at the same clip.

Figure 1: Average Tariff Rates by Month for All Imports

Source: US International Trade Commission, as of January 31, 2026. Data covers January 2024 – November 2025.

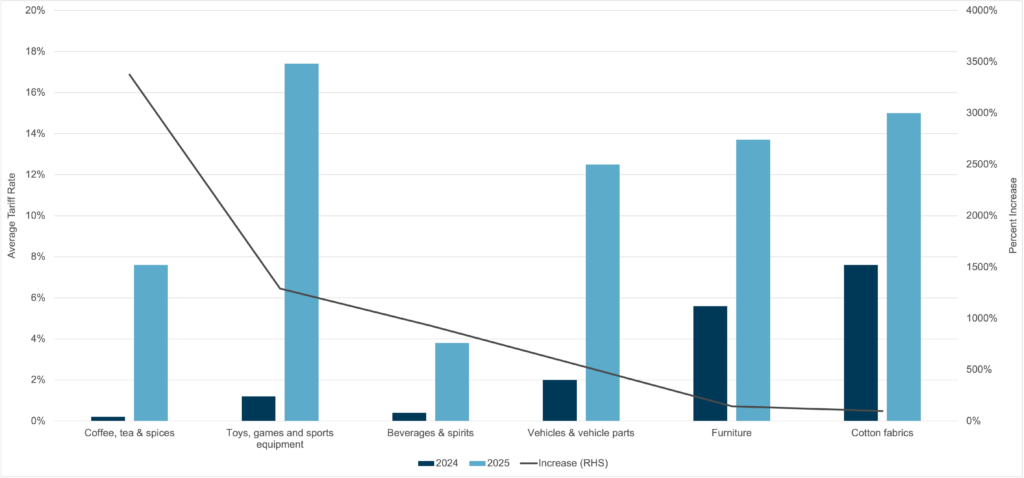

And while average tariff rates have been rising, tariffs haven’t affected all goods equally. Categories seeing the biggest impact include food and beverages, electronics, clothing, toys and furniture.

Figure 2: Average Tariff Rates for Key Imports: 2024 vs. 2025

Source: US International Trade Commission’s Harmonized Tariff Schedule, as of January 31, 2026. Categories represent the HTS commodity code. Data covers January 2024 – November 2025.

The full impact of the past year’s cost increases has not always been reflected in end-market pricing in real time. In 2025, many companies mitigated near-term price pressure by accelerating purchases, aiming to lock in lower costs ahead of expected tariff changes. As costs rose, many companies found it difficult to raise prices commensurately due to consumer resistance, competitive dynamics and, in some cases, regulatory or political scrutiny. The result was widespread margin erosion and reduced company profitability, even as reported inventory values increased.

Companies that update standardized cost systems annually are particularly vulnerable in this environment. For them, cost inflation that accumulates over several quarters may not be fully recognized until well after inventory has been purchased, produced and distributed.

Reciprocal tariffs and broad product coverage mean that relatively few consumer-facing companies can fully avoid tariff exposure. Even companies that face limited direct exposure must manage substantial indirect effects like supplier passthroughs, freight surcharges and currency impacts. As a result, many companies have attempted to reconfigure supply chains and inventory strategies in real time.

One initial response has been early purchasing and over-inventorying to hedge anticipated tariff increases. While this approach provided temporary insulation from rising costs and delayed price increases in 2025, it also increased balance-sheet exposure and raised the risk of holding high-cost inventory into periods of weaker demand or tighter liquidity. A strategy intended as a bridge to a more stable era of tariffs and costs has, in many cases, extended the period of divergence between cost basis and realizable value.

Looking ahead, the pricing environment seems likely to shift. As companies work through pre-tariff inventory and face mounting cost pressures, they are likely to pass through price increases more fully and focus on rebuilding gross margins. As prices increase, the impact could result in lower demand as the consumer price elasticity will be tested.

Where the Stress Is Most Acute

The impact of these dynamics has been uneven. Industrial companies, particularly original equipment manufacturers (OEMs), generally have not been hit quite as hard as consumer-facing businesses. Many industrial firms benefit from regional production, established exclusions or supply chains that are less concentrated in tariff-exposed jurisdictions. Although China-centric supply chains remain common in machinery and equipment, higher margins and longer contract cycles can provide some buffer.

By contrast, retailers face greater challenges. They tend to have broad tariff exposure with few exclusions, limited pricing power and high SKU counts, making inventory valuation particularly complex. Value-oriented retailers have been hit disproportionately, in part because their customers are least able to absorb price increases.

Company size also plays an important role in resiliency in this environment. Larger companies are generally better positioned to renegotiate supplier pricing, diversify sourcing and absorb volatility. Smaller firms face higher input costs, less pricing power, weaker liquidity and limited flexibility to rework inventory portfolios. As a result, the gap between cost and realizable value tends to widen fastest among small and mid-sized businesses.

Some large retailers have attempted to push tariff and freight risks upstream to suppliers. For example, one retailer that historically picked up products in China now requires suppliers to deliver goods to Los Angeles at a fixed price. This change effectively transfers the risk of higher tariffs and freight costs to the supplier, often at the expense of supplier margins or financial stability. While this strategy can protect retailer margins in the short term, it may ultimately reduce supplier resilience and increase disruption risk.

Other retailers, particularly smaller or highly leveraged players, are weighing whether to continue operating under the new cost structure at all. For these companies, inventory decisions have become existential rather than tactical. The cookware industry illustrates the severity of the challenge: Tariffs on steel and aluminum have surged to as high as 50%, forcing manufacturers to consider alternative materials, attempt onshoring or accept structurally lower margins.

Seasonal categories such as patio furniture face an additional layer of risk. For companies in this sector, high freight and tariff burdens have combined with narrow selling windows and demand uncertainty. In these conditions, spring and summer inventory effectively becomes a stress test for solvency, not just profitability. The National Retail Federation estimated that tariffs could drive $8.5 to $13.1 billion in annual cost increases for U.S. furniture consumers overall.

A Shifting Picture of Valuation and Recovery

These conditions have meaningful implications for the ways inventory should be valued. Historically, inventory has often been treated as a relatively reliable asset, with liquidation values modeled at a discount to cost. In today’s environment, companies can’t necessarily make that assumption.

Higher-cost, slower-moving inventory with uncertain exit pricing introduces greater downside risk. Lower turnover combined with shrinking margins increases capital strain and reduces the time available to course correct.

Gross margin variability at the SKU level further complicates valuation. Tariffs and freight costs do not affect all products equally, and margin compression is often concentrated in specific categories. Portfolio-level averages can obscure significant pockets of underperformance, leading to overly optimistic recovery assumptions.

Operational Signs of Trouble

Certain operational signals can indicate when inventory valuation risk is becoming acute. Expanding variance accounts and reduced or unclear profitability by SKU often suggests that cost systems are struggling to keep up with reality. When companies cannot confidently identify which products are driving or destroying margin, inventory decisions become reactive rather than strategic.

Another warning sign is the simultaneous presence of prolonged inventory holding periods and stock-outs. This combination often reflects poor alignment between purchasing, pricing and demand forecasting. High-cost inventory may sit unsold, while capital constraints prevent timely replenishment of better-performing items.

Several metrics are particularly key to monitor in this environment:

- Gross margin variability by product line.

- Inventory aging at cost versus expected exit price.

- Tariff dollars paid as a percentage of revenue and margin.

Tracking these indicators over time can help identify when cost-basis assumptions are diverging from economic reality, and when intervention may be required.

Takeaways for Companies

For operating companies, navigating the current environment requires faster and more disciplined responses. Resetting pricing toward a new margin normal is essential, even if it must be selective. Regional pricing, targeted increases and differentiated strategies by channel or customer segment may be more sustainable than across-the-board hikes.

Portfolio-level margin management also can help. Companies that model their inventory portfolios dynamically are better positioned to make timely adjustments, including accelerating markdowns where appropriate and reallocating capital toward better-performing products.

In addition, a clear-eyed assessment of how inventory supports recovery value is increasingly necessary. In some cases, repricing via new products may be more effective than attempting to rehabilitate legacy SKUs burdened by high costs. Increased SKU rationalization can reduce complexity and free up working capital.

Finally, expanding and developing supplier networks across multiple jurisdictions can provide much-needed flexibility. Over time, this sort of diversification strategy can reduce exposure to any single tariff regime and improve negotiating leverage.

Takeaways for Lenders

For lenders, the changing nature of inventory risk demands a more granular, forward-looking approach. Inventory that appears adequately margined on paper may be vulnerable to prolonged holding periods or forced liquidation at steep discounts. While borrowers often remain anchored to cost, lenders must increasingly base decisions on what inventory can realistically generate in a stressed sale scenario.

Greater variability in gross margins at the SKU level also complicates underwriting. Borrowing bases that rely on blended advance rates may overstate availability if a significant portion of inventory is unprofitable or mispriced. As a result, lenders may need to incorporate more SKU-level analysis, bifurcated advance rates and scenario modeling into their monitoring processes.

In short, lenders should treat inventory as a dynamic risk asset, not a static balance-sheet figure. This shift means changing the focus from historical cost to realizable value and recognizing that the relationship between the two is becoming less stable.

A Necessary Shift in Perspective

Companies and lenders alike must adjust to a new reality in which tariffs and supply-chain changes are not just cost issues but valuation issues. As cost basis and realizable value diverge, recovery outcomes will depend on how quickly stakeholders adjust expectations, metrics and decisions. Companies that cling to historical assumptions risk overstating asset values and delaying necessary action.

The next cycle of distress is likely to be defined less by leverage and more by mispriced inventory. In that environment, the ability to evaluate inventory clearly may be the decisive factor in determining recovery outcomes.