The Rise of AI and the Need for Flexible Financing

Increased Power Needs Lead to Supply-Demand Challenges

This article is featured in our 2026 Global Asset Insights Report. Access the full report to get insights across sectors on the outlook for 2026 and themes impacting the ways companies do business. Read the report >

Moody’s predicts that global data center investment will reach at least $3 trillion over the next five years, with a continued push to shorten new build delivery timelines.1

Companies are investing heavily in real estate, data centers, power sources and other in-demand resources that currently face years of lead time for delivery due to the significant increase in total power center inventory across the U.S.2 In 2025, nearly $200 billion in total debt was raised for data center development. While much of the financing focuses on purchasing real estate, power generation equipment itself often requires a separate financing solution. This boom is driving significant demand for lending and equipment financing capabilities, with the assets powering the revolution representing billions in equipment value and thus needing flexible, collateral-based financing solutions.

Infrastructure groups and tenants looking to create a new center often aren’t able to secure funding until power is provided, but power suppliers cannot commit until financing is in place, creating a chicken or egg scenario for lenders. All three major players in this development—infrastructure groups, lenders and power suppliers—are working on different timelines, creating a massive financing gap.

“Demand for prime power elements continues to increase. There is a strong opportunity to help clients value and finance these assets to ensure long-term success and establish backup power needs. As markets continue to develop and appreciate, so does the equipment required to keep operations running smoothly.”

—ZAC DALTON, HEAD OF INDUSTRIAL CLIENT COVERAGE & ORIGINATIONS

Given these tricky dynamics, and that projects are often years away from completion on the manufacturer’s side, companies require not only the right resources but financing that allows them to move quickly to secure the order. In the near term, this includes:

- Front End: Providing appraisals, lending and equipment financing capabilities

- Back End: Procure, buy and sell power equipment while properly monetizing assets

Prime vs Backup Power Elements

- Prime Power: The main source of power on the site, designed to operate continuously over a long timeframe

- Backup Power: Supplies power to equipment if prime power requires additional support, or if it is lost

As prime power orders are completed, we anticipate that backup power will become a more valuable commodity. All of the power generating equipment used is tangible, appraisable and retains significant value in the short-term—creating a perfect opportunity for ABL. As construction projects scale up capacity in phases, ABL can provide a unique solution in the form of equipment-specific financing and revolving lines of credit that can scale with the project. However, the rapid pace of changing technologies and long production lead times in equipment manufacturing raise more questions over the long term.

Risks and external factors still remain that could hamper infrastructure expansion—creating winners and losers among companies and lenders. The potential for state and municipal regulations, grid power and connectivity issues, criticism of nuclear capabilities and pricey national gas contracts continue to create uncertainty about power availability and demand. This means long-term success lending in this space will depend on a strong understanding of the infrastructure supply chain, expertise in equipment financing and adaptability to account for a range of potential industry risks.

What Fuels the Power Boom?

- Natural Gas

- Renewable Energy (solar, wind, hydro)

- Nuclear

- Coal

- Diesel

Companies able to bring together both the resources needed to power the increasing demand and liquidity needed to ensure continued growth will succeed in this fast-moving environment.

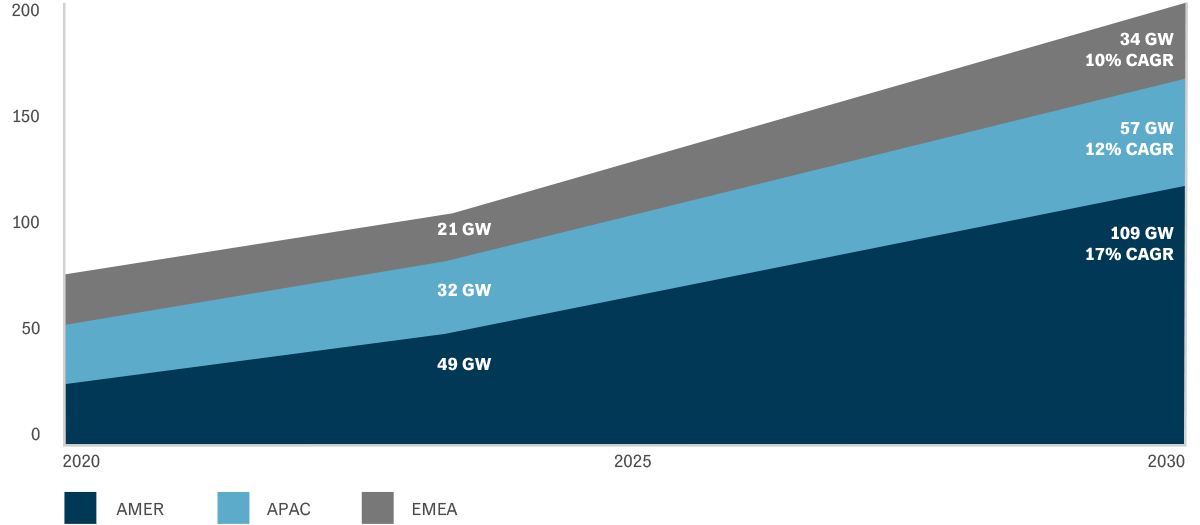

Nearly 100 GW of new data centers will be added between 2025 and 2030, doubling global capacity

Global Supply Forecast by Region (GW)

Source: JLL Research, 2025. Supply totals include co-location, built-to-suit, hyperscale owner-occupied and on-prem.

Want to read more insights like this? This article is featured in our 2026 Global Asset Insights Report. Access the full report to get insights across sectors on the outlook for 2026 and themes impacting the ways companies do business. Read the report >

- Moody’s, Data centers: Managing risk amid a market boom.

- CBRE, High Demand, Power Availability Delays Lead to Record Data Center Construction.