TV and Film Production: Catastrophic Triple Impact for the Crown Jewel of the U.K.’s Creative Industries

Lights, Camera, No Action

The TV, film production and broadcasting sector is undergoing seismic shifts in the United Kingdom, marked by declining revenues, rising insolvencies and structural disruption across traditional and digital platforms. The U.K. has long stood as a global leader in the sector, second only to Hollywood, with 86% of its film and high-end prestige TV productions originating from major U.S. studios. This success has been built on the foundations of a highly skilled, mobile labour pool, specialised supply chains in lighting, cameras, IT, rigging, and set production and world-class studios – all of which have made the U.K. a magnet for international productions. Now, with evident rationalisation, consolidation and dwindling TV advertising, AV and broadcast sector businesses are beginning to suffer. Versatility within the sector and the fusion of skills and innovation from sectors such as gaming are key to future innovation and international competitiveness.

However, the industry now faces a perfect storm of challenges:

- The lingering effects of COVID-19 pandemic shutdowns

- The far-reaching impact of U.S. writers’ and actors’ strikes (the first in 60 years)

- A significant advertising slump and content recycling trend

These combined forces have created a landscape of uncertainty, job losses and financial strain across the sector.

Lingering Effects of COVID-19

During the COVID-19 shutdowns, the Coronavirus Business Interruption Loan Scheme (CBIL) and equipment lessor payment holidays in the U.K. largely supported the sector’s supply chains. Post pandemic, the financial implications and burden on the loans taken during this period have spiralled, with a ten-fold increase in the base interest rate from 0.5% to 5%. In addition, a workforce dominated by self-employment found itself adrift to find government support or alternative employment to make ends meet.

A short-term boom emerged after Covid restrictions eased, leading to a rush for studio space. However, this was undercut as streaming services including Disney, Netflix and Warner Bros significantly cut back on spending until their heavily loss-making streaming services become profitable, following significant drops in subscriber numbers being recorded following the pandemic boom.

U.S. Strikes Impact U.K. Industry

From May to October 2023, the Writers Guild of America (WGA) went on strike over a labour dispute with Alliance of Motion Picture and Television Producers (AMPTP). From July to November 2023, the American actors’ union Screen Actors Guild – American Federation of Television and Radio Artists (SAG-AFTRA) was also on strike over a labour dispute with the Alliance of Motion Picture and Television Producers (AMPTP).

There were multiple reasons for the strikes but artificial intelligence (AI) was one of the main concerns highlighted. AI is revolutionising the AV and broadcasting sector by enhancing automation, personalisation and analytics. But alongside these user experience enhancements lie deep concerns over the use of AI in damaging artist intellectual property and the associated issues of ensuring proportionate remuneration. The combined impact of these two strikes resulted in the loss of 45,000 jobs in the U.S. and sent a shock wave to the U.K. resulting in a second shutdown event quickly after activity started to improve post COVID.

Advertising Slump & the Rise of Content Recycling

The TV advertising market in the U.K. had its biggest annual decline since 2009 in 2023 since and is forecasted to contract by a further 7% in 2024. TV advertising isn’t translating into sales like it once did, so fewer companies are advertising through TV and channels can no longer rely on advertising spend as a revenue driver.

Overall, younger generations watch less TV and traditional broadcasters are scrambling to reinvent themselves in the digital space as attraction to TikTok, Instagram, Facebook and Google continues to grow. As ad revenues decline, so does the level of new commissions from U.K. broadcasters who have a rich store of content to recycle that drives a reduction in commissions as advertising revenues fall.

For example, the BBC has registered a real term fall in income of close to a third since 2010 which is a difference of more than £1 billion a year. The corporation is cutting 500 jobs in 2024 following real term decline in its licence fee revenue over the past decade. In 2023 alone, over 500,000 households cancelled their licence fee. The BBC is coming under increasing competitive pressure from global streaming services.

Workforce Impacts & Retention Risks

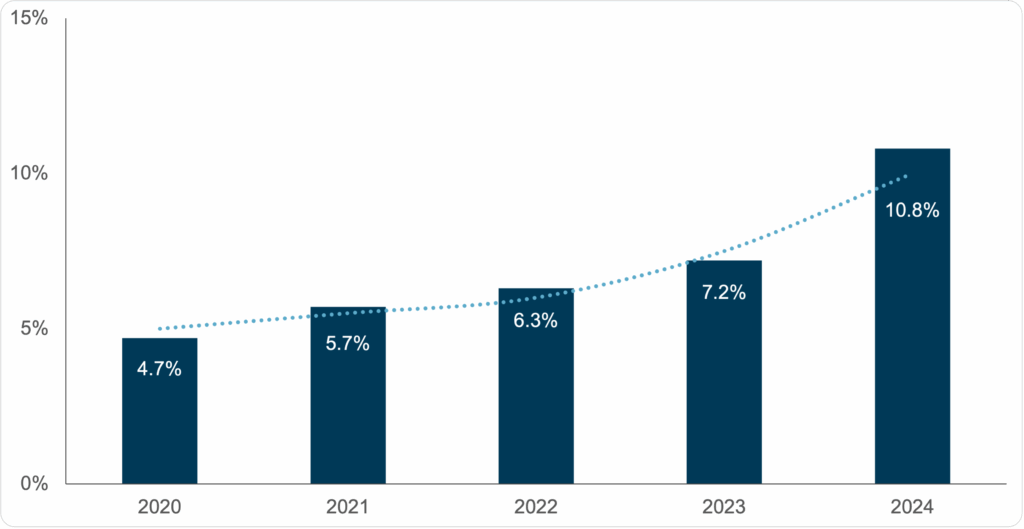

Insolvencies in the sector have increased, with notable recent auctions including Arena Television, Procam Take2, Anna Valley, Televideo and Video Europe. There is evidence of consolidation and rationalisation in the U.K. sector with the recent EMG Gravity merger and the Pro Motion Hire, Stage 50, Shift 4 and Presteigne business asset sales from an insolvency process.

The number of administrations in the media and tech sector has been trending upwards since 2020. The sector previously tracked around 4% to 5% of all administrations. Critically, it is now at 11% of all administrations for the first six months of 2024, indicating a significant increase in financial distress.

According to a 2024 survey by the Broadcasting, Entertainment, Communications and Theatre Union (BECTU), 52% of the U.K.’s film and TV workforce are still out of work. The proportion of those out of work is high across all sectors, including film (52%), TV drama (51%), unscripted TV (57%) and commercials (53%). Only 6% say they have seen a full recovery in their employment since the U.S. industry strike ended.

The BECTU survey also highlighted that nearly a quarter of respondents said they did not see themselves working in the industry in the next five years. Stemming a mass skills exodus from the U.K. sector is imperative, alongside moves to encourage production on U.K. soil. Failure to do so could see an even greater rise in insolvencies. The U.K. government has introduced tax breaks and increased financial support to the creative sector in the 2025 budget to encourage more film and TV productions.

Impact on Asset Values

Given the high capital expenditure associated with entertainment production, the used equipment market offers significant cost savings, which is especially appealing to smaller production companies, educational institutions and those operating in second tier markets like independent productions and lower income international filming locations.

The used entertainment broadcasting and production equipment market is integral to the broader entertainment and events industry in the U.K. and globally, providing a more accessible entry point for small to medium enterprises and new entrants to the industry. The proliferation of digital technologies and the demand for production of live events and broadcasts has sustained a robust secondary market.

Production assets are mostly universal in nature and as such will command worldwide demand and a global reach in a work-out situation. While price erosion in broadcasting equipment exists in the U.K. markets, it is less significant in other large film markets across Europe, Middle East and Asia where demand is stronger. Similarly, the increase in televised events in the Middle East and Africa have spawned a new calibre of operators who create demand for used broadcast equipment. Although asset values are not as high as they were in the post-pandemic boom, there is still strong demand for used broadcasting and production equipment across the globe.

To learn more about how Gordon Brothers can support your business through asset recovery, valuation or disposition strategies, reach out to one of our experts or contact us.